Key Highlights

If you can’t make a mortgage payment, act fast and don’t wait for missed payments to pile up.

Review your financial hardship, income, and bills so you know what you can realistically afford.

Contact your mortgage lender or mortgage servicer early to ask about available solutions.

Assistance programs such as forbearance, repayment plans, and loan modification may help you avoid foreclosure.

Missing payments can hurt your credit score, so quick action matters.

In some cases, selling, renting, or other relief options may help you keep control.

Introduction

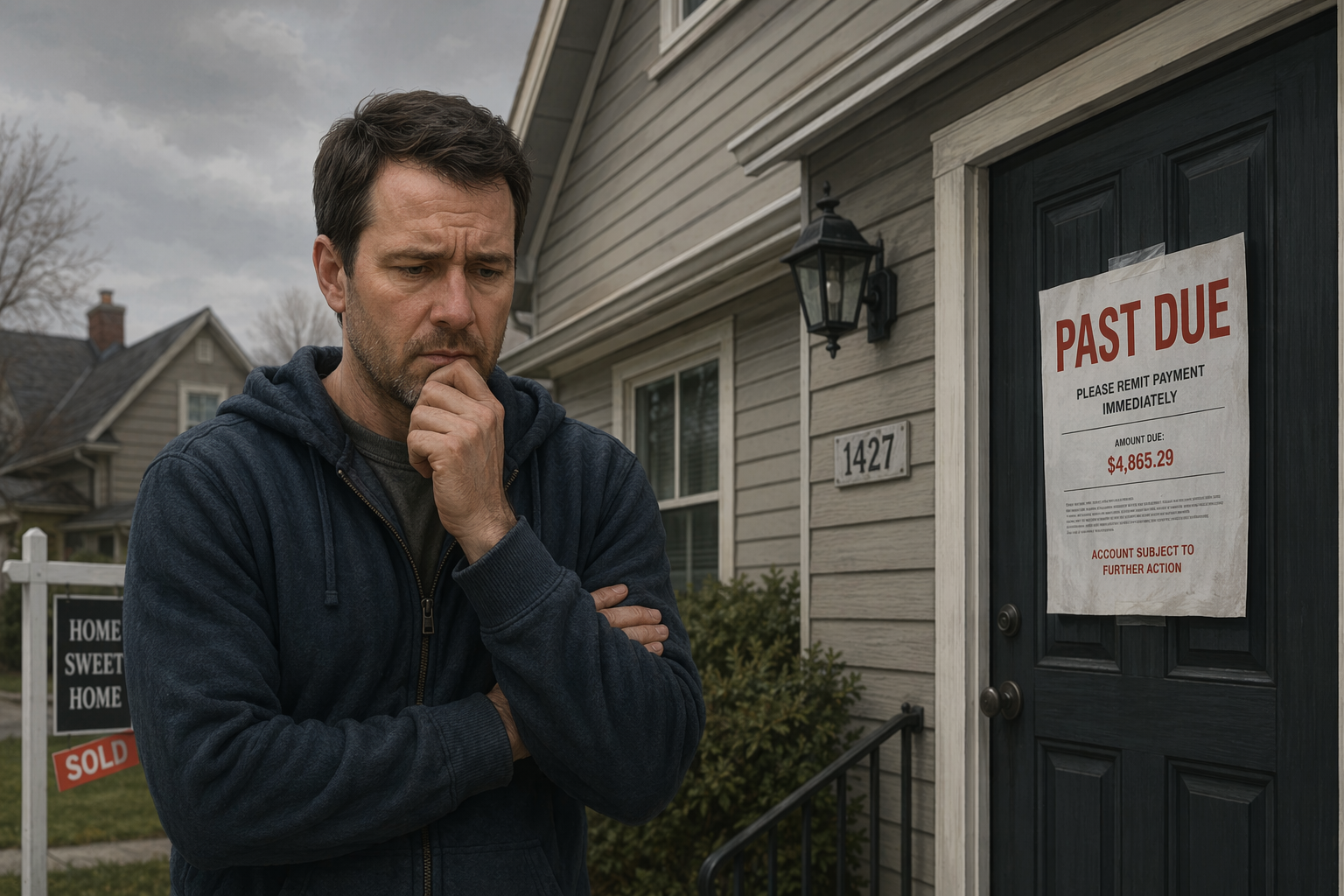

If you’re worried about making your next mortgage payment, you’re not alone. A sudden financial hardship, loss of income, or rising bills can make a mortgage loan feel harder to manage than expected. The good news is that early action can open more options. Instead of waiting until the problem grows, you can take a few practical steps now. Start by spotting warning signs, reviewing your finances, and preparing to speak with your lender before the situation gets worse.

Recognize the Warning Signs of Mortgage Trouble

Mortgage trouble often starts before you actually miss a payment. You may notice that your hardship is forcing you to choose between housing and other essential bills. If that keeps happening, the risk of missed payments goes up quickly.

Once payments fall behind, the foreclosure process can move closer, and your credit can take a hit. Reaching out early to your lender or a housing counselor may help you explore options like loan modification before your account becomes more serious.

Early indicators you might fall behind on payments

Sometimes the first warning sign is simple: your monthly budget no longer works. If your income dropped, your property tax or insurance costs went up, or another major bill appeared, the due amount on your mortgage loan may start feeling out of reach. That is the moment to pay attention.

You may be at risk if you notice any of these signs:

You are using savings to cover regular bills each month.

You can only make part of the due amount.

Your income has changed because of job loss, illness, or divorce.

You are falling behind on other debts while trying to protect the mortgage loan.

At that stage, your first step should be to review your financial situation right away. Write down your income, fixed expenses, and upcoming bills. That gives you a clearer view of whether the problem is short term or long term and helps you prepare before missed mortgage payments begin.

Understanding how payment difficulties lead to foreclosure

When you miss a payment, the problem usually grows in stages. A short delay may begin with a grace period, but after that, late fees can be added. Once you reach 30 days late, the mortgage company may report the delinquency to credit bureaus, which can damage your credit score.

If the account keeps falling behind, the risk increases. Around 90 days late, the loan may be treated as being in default, and the lender may warn that the foreclosure process is coming. By about 120 days late, foreclosure action may begin, depending on the rules in your area.

Assess Your Current Financial Situation

Before you call anyone, take a close look at your financial situation. You need to know how much income is coming in, what your fixed expenses are, and whether your current loan amount is still manageable. That gives you a stronger starting point.

A simple budget review can also support better debt management. When you understand what you can cut, postpone, or repay later, you can speak more clearly with your lender. The next two steps focus on reviewing numbers and gathering the documents you may need.

Reviewing your income, expenses, and upcoming obligations

Start with a plain, honest snapshot of your money. List your income, regular expenses, and anything due soon. This helps you see whether your mortgage trouble is caused by a temporary gap or a longer-term issue. It also shows what payment range may actually fit your financial situation.

Focus on items such as:

Current income from work, benefits, or other sources

Regular expenses like utilities, food, and transportation

The monthly mortgage loan amount and escrow-related changes

Upcoming obligations such as insurance, property tax, or medical bills

Other debt payments that affect your cash flow

Once you write everything down, look for patterns. Are rising expenses the problem? Did loss of income create the pressure? This review helps you explain your situation clearly and prepares you to discuss realistic solutions instead of guessing during a stressful phone call.

Gathering key documents before seeking mortgage help

Having paperwork ready can make the process smoother. Many lenders ask for proof of hardship and a clear picture of your finances before discussing loan modification, a repayment plan, or other mortgage loan relief. Organized records can also help if you later explore a new mortgage or refinancing.

Try to gather:

Recent pay records or other proof of income

Monthly bills, bank statements, and mortgage statements

A written explanation of your hardship

Your credit report so you understand any recent damage

These documents help you answer common questions from the servicer. They may want to know what caused the problem, whether it is temporary, and how you plan to recover. The more prepared you are, the easier it is to move the conversation toward practical options rather than delays.

Communicate Promptly with Your Mortgage Lender

Your first contact should usually be your mortgage lender or mortgage servicer. As the borrower, you want to reach out as soon as you know the payment may be a problem. Waiting can limit the choices available to you.

Talking to the mortgage company does matter. In many cases, lenders are more willing to discuss solutions when you contact them before the account becomes seriously delinquent. The next sections cover how to start that conversation and what help may be available.

How to reach out and what to say when you can’t pay

A direct, calm conversation is often the best place to begin. Contact your mortgage servicer by phone, and if needed, follow up by email or letter. As the borrower, you should explain what changed, when the hardship began, and whether you think the problem is temporary or lasting.

Be ready to cover these points:

Why you cannot make the next payment

Whether the hardship involves loss of income, illness, or another event

What amount you may be able to pay now

Whether you want to keep the home

Good communication also means keeping records. Write down dates, times, names, and what was discussed. If the lender asks for documents or gives deadlines, respond quickly. Clear notes can help you stay organized and show that you are making a good-faith effort to solve the problem.

Options your lender may offer if you’re struggling

If you speak with your lender early, several paths may be discussed. Some options are meant to help you keep your home, while others are designed to reduce the damage if staying is no longer realistic. The right fit depends on whether your hardship is short term or permanent.

Possible solutions may include:

A repayment plan that spreads past-due amounts over time

Forbearance that pauses or reduces payments for a period of time

Loan modification that changes the terms to lower the monthly burden

A short sale if the home must be sold for less than owed

A deed in lieu of foreclosure as a last resort

Ask how each option affects your monthly payment, mortgage debt, and timeline. Also ask whether extra payments, a lump sum, or added balance at the end of the loan may be required. Clear questions help you compare choices with fewer surprises.

Explore Programs and Relief Options for Homeowners

If your servicer cannot solve everything right away, you may still have other mortgage relief paths to explore. Assistance programs from government programs, housing agencies, and lenders can help homeowners understand what may apply to their situation.

Some options are aimed at temporary hardship, such as forbearance, while others may support longer-term changes. The key is to learn what is still available and who can guide you. That often starts with trusted federal housing resources and approved counseling support.

Government and lender assistance programs in the United States

Trusted help is available, and you do not need to guess where to begin. The Consumer Financial Protection Bureau provides centralized housing information, while HUD can help you find approved housing counseling services. These counselors are often free or low cost and can explain your options clearly.

You may also want to check whether your loan is connected to federal or major housing systems. Depending on your mortgage, resources related to HUD, FHA, VA, Freddie Mac, or Fannie Mae may point you toward available relief or servicing guidance.

Start with legitimate sources and your servicer. If you are having trouble reaching the lender or understanding the process, a housing counseling agency can help you prepare paperwork, prioritize debts, and ask better questions. That support can make a stressful situation feel more manageable.

Understanding forbearance, loan modification, and refinancing

These three options are often discussed together, but they work very differently. Forbearance is usually temporary. Loan modification changes the terms of your loan on a lasting basis. Refinancing replaces your current loan with a new loan, usually to get a lower payment through a different interest rate or longer term.

Here is the basic difference:

Forbearance pauses or reduces payments for a limited period

Loan modification permanently changes terms of your loan

Refinancing replaces the old loan with a new one

Refinancing often works best when credit and home equity are still strong

Each option has trade-offs. Forbearance does not erase what you owe, and repayment starts after the forbearance period or at the end of the forbearance. Modification can increase total interest over time. Refinancing may involve fees and may be harder after missed payments have affected your credit.

Common Mistakes to Avoid When Missing a Mortgage Payment

When stress builds, it is easy for a borrower to freeze or hope the problem will disappear. That can lead to bigger trouble. Ignoring the issue may push the loan closer to default and increase mortgage debt through fees and added charges.

Another major mistake is trusting the wrong source for help. Bad advice, delayed action, or a scam can make foreclosure more likely. The next two sections cover why quick contact matters and how to protect yourself while looking for relief.

The risks of ignoring mail or delaying contact

Ignoring letters from your lender is one of the most damaging choices you can make. Those notices may include deadlines, requests for documents, or warnings that your account is moving toward default. If you set them aside, you may miss a chance to act before the situation worsens.

Delay also gives missed payments more time to grow. Late fees, added interest, and default-related property charges can raise what you owe. If no solution is reached, foreclosure may move forward and become harder to stop.

If the process is already advanced or you feel overwhelmed, ask for help right away. A HUD-approved housing counselor can explain your options, and legal aid may help if you are at risk of losing your home or facing complicated state procedures. Early support can protect your rights.

Avoiding scams and misinformation about mortgage relief

Mortgage trouble can make anyone vulnerable to bad actors. Some companies promise they can stop foreclosure if you pay upfront. That is a major red flag. No one can guarantee that a lender will stop the process, and advance-fee promises are often part of a scam.

Watch for warning signs such as:

Demands for money before any real help is provided

Guarantees of a loan modification

Pressure to avoid your mortgage servicer

Advice that sounds secret, rushed, or too good to be true

Stick with trusted sources. Contact your lender or mortgage servicer directly, and use information from the Consumer Financial Protection Bureau, HUD-approved counselors, or legal aid if needed. Honest help should be clear about costs, realistic about outcomes, and never promise a result no one can control.

Conclusion

In conclusion, facing difficulties with mortgage payments can be daunting, but taking proactive steps is essential. Recognizing the warning signs early, assessing your financial situation, and communicating promptly with your lender can make a significant difference in navigating your options. Exploring assistance programs and being aware of common pitfalls can empower you to make informed decisions that safeguard your home ownership. Remember, you are not alone in this process, and seeking help is a strong step toward financial stability. If you're feeling overwhelmed, don’t hesitate to reach out for support.

Frequently Asked Questions

How will missing a mortgage payment affect my credit score?

Missing a mortgage payment can hurt your credit score once the account becomes late enough to be reported. Missed payments may appear on your credit report, and repeated delays can push the loan toward default. The longer the problem continues, the greater the likely damage.

Who can provide legal assistance if I’m at risk of losing my home?

If you are facing foreclosure or serious mortgage debt problems, legal aid may be able to help. You can also speak with a HUD-approved housing counselor for guidance and referrals. Both can help you understand your options and respond before you lose important time.