Key Highlights

Unemployment benefits can serve as a temporary financial bridge to help you make mortgage loan payments and work toward foreclosure prevention.

Various government programs and unemployment insurance provide mortgage relief options for homeowners facing financial hardship.

If you're struggling, it's crucial to contact your lender immediately to discuss your situation and explore available assistance.

HUD-approved housing counseling agencies offer free guidance on navigating your options and communicating with your servicer.

Understanding the foreclosure timeline in your state is key to acting quickly and effectively.

Prioritizing mortgage payments over other unsecured debts is a critical step in avoiding foreclosure during unemployment.

Introduction

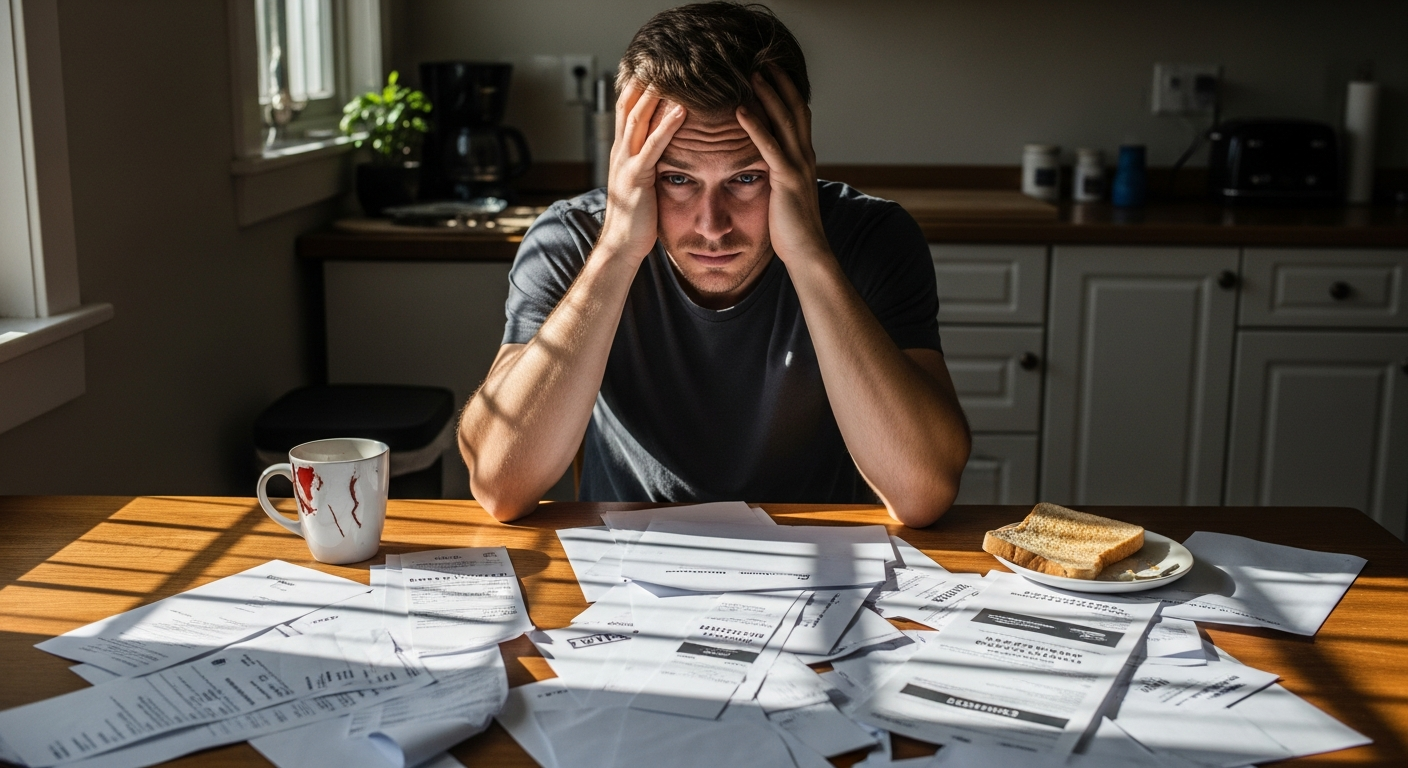

Losing a job can be incredibly stressful, especially when you have a mortgage to pay. Suddenly, the threat of foreclosure becomes a real and frightening possibility. If you're in this situation, you might be wondering if unemployment benefits can help you stay afloat. The good news is that these benefits, along with other resources, can be a vital part of your foreclosure prevention strategy. This guide will walk you through how to navigate this financial hardship and use the support available to protect your home.

Understanding the Risk of Foreclosure for Unemployed Homeowners

The risk of foreclosure increases significantly after job loss. Without a steady income, keeping up with mortgage payments can feel impossible, putting your home in jeopardy. These difficult financial times can quickly escalate, leading to a situation where you're facing legal action from your lender.

It's important to know your rights and the foreclosure laws in your state, as they vary. Understanding the process and the resources available, like unemployment insurance, can empower you to take proactive steps. Let's look closer at why job loss is a major trigger for foreclosure and what warning signs to watch for.

Why Job Loss Increases the Likelihood of Foreclosure

When you lose your job, your primary source of monthly income disappears. This sudden financial shock makes it challenging to cover essential expenses, especially large ones like your mortgage payment. Even with unemployment compensation, the amount you receive is often much less than your previous salary.

This gap between your reduced income and your existing financial obligations puts you at a high risk of default. A mortgage is typically the largest monthly expense for a homeowner, and missing even one payment can start a domino effect that's difficult to stop.

Your entire financial situation is thrown into disarray. Without sufficient income, you may have to choose between paying your mortgage and buying groceries. This is why unemployment is one of the leading causes of homeowners falling behind on their loans and ultimately facing foreclosure.

Common Warning Signs of Possible Foreclosure

Recognizing the early foreclosure warning signs is crucial for taking timely action. Don't wait until the situation is dire. Being proactive can make all the difference in saving your home from the foreclosure process.

Are you experiencing any of the following? These are red flags that you might be heading toward trouble with your monthly payments.

Your credit card debt is becoming unmanageable.

You've started using credit cards for essential purchases like groceries.

It's getting harder to pay all your monthly bills on time.

You've received a "Demand Letter" from your lender.

If these signs sound familiar, it’s time to act. A demand letter, in particular, is a serious indicator that your lender is prepared to begin foreclosure proceedings. A declining credit score can also signal mounting financial pressure.

The Foreclosure Timeline in the United States

The foreclosure timeline doesn't happen overnight, but it can move faster than you think. The exact process and duration vary by state, but it generally follows a predictable pattern. From the first missed payment, your mortgage company will begin to take action.

Initially, your loan servicer will contact you by phone or mail. As you miss more payments, the communications become more serious, leading to a formal demand letter. This is a critical window to engage in loss mitigation discussions. If no arrangements are made, the case is sent to attorneys, and you'll face a foreclosure court.

What Are Unemployment Benefits and How Do They Work?

Unemployment benefits, also known as unemployment compensation, are a form of temporary financial assistance for workers who have lost their jobs through no fault of their own. This support is provided through state-run unemployment insurance programs, funded by taxes paid by employers.

The purpose of these benefits is to provide a partial income replacement while you search for new employment. This money can help you cover essential living expenses, including your housing costs, bridging the gap until you get back on your feet. Next, we will explore the specifics of these programs, from eligibility to payment calculations.

Overview of State Unemployment Insurance Programs

Unemployment insurance is a joint federal-state partnership, but the programs themselves are administered at the state level. This means that the rules, benefit amounts, and duration of assistance can vary significantly from one state to another. These government programs are designed to be a safety net for workers during periods of joblessness.

When you receive payments, this unemployment income can be used for any of your living expenses. For a homeowner, this can be a lifeline, providing the funds needed to make a mortgage payment and prevent a default. These state programs are a key resource for maintaining financial stability.

By providing this temporary income, the system helps you keep up with your obligations. This support can be the crucial factor that allows you to continue paying your mortgage while you search for a new job, directly helping you avoid the threat of foreclosure.

Eligibility Criteria and Application Process

To qualify for unemployment benefits, you must meet specific eligibility requirements set by your state. Typically, you need to have lost your job through no fault of your own, such as a layoff. You must also meet criteria related to your work and earnings history.

The application process usually involves providing documentation of your past employment and gross income. You may need to supply information from your tax returns or pay stubs. Once you apply, you must also be able and available to work and actively seeking new employment.

Common eligibility requirements include:

Being unemployed through no fault of your own.

Meeting your state's requirements for time worked or wages earned.

Being able and available to work.

Actively looking for work each week you receive benefits.

How Unemployment Payments Are Calculated

The amount of unemployment compensation you receive is based on your previous earnings. Each state has its own formula for calculating benefits, but it's generally a percentage of your average gross income during a specific "base period," which is typically the last four or five calendar quarters you worked.

States set a weekly minimum and maximum benefit amount. Your payment will fall somewhere in this range, depending on your past wages. It’s important to remember that this amount will likely be significantly lower than the paycheck you were used to receiving.

Keep in mind that unemployment benefits are considered taxable income by the IRS and must be reported on your federal tax return. You can often choose to have federal income tax withheld from your payments to avoid a large tax bill later. This income, while reduced, is still a factor when lenders consider you for mortgage assistance.

Can Unemployment Benefits be Used Toward Mortgage Payments?

Yes, you can absolutely use your unemployment benefits to make your mortgage payment. There are no restrictions on how you use this money; it is intended to help you cover your essential living expenses, and your housing payment is one of the most important. For many, this is the primary purpose of the funds.

Using your benefits for monthly mortgage payments can provide the stability needed to stay in your home while you search for a new job. However, since the benefit amount is limited, you will need to budget carefully. We will now discuss how to allocate these funds and what limitations to consider.

Guidelines for Allocating Unemployment Checks to Household Expenses

When you start receiving unemployment compensation, your first step should be to create a crisis budget. Your financial situation has changed dramatically, and you need a clear plan for your limited available cash. Prioritizing expenses is essential.

Housing should be your top priority. After covering immediate needs like food and healthcare, your mortgage payment should come before other monthly bills like credit cards or personal loans. Your unemployment benefits provide the cash flow to make these critical payments.

To manage your funds effectively:

Create a list of all your monthly bills and income sources.

Prioritize your mortgage, utilities, and food above all else.

Cut back on non-essential spending like entertainment, subscriptions, and dining out.

Use your unemployment benefits to cover these top-priority expenses first.

Limitations and Considerations for Using Benefits on Housing

While unemployment compensation is a vital tool, it's often not enough to cover a full house payment on its own, especially if you live in a high-cost area. The benefit amount is only a fraction of your previous income, which can create a significant budget shortfall.

This is why communication with your loan servicer is critical. Informing them of your financial hardship and your reliance on unemployment income can open the door to temporary relief options. They may be able to offer a forbearance or another plan where your partial payments are accepted.

Don't assume your unemployment check will solve the problem entirely. View it as a component of a broader strategy that includes cutting expenses, seeking other assistance, and working with your lender. It's a temporary solution to help you through a difficult period, not a long-term fix for an unaffordable mortgage.

Prioritizing Your Finances During Unemployment

When your financial situation changes due to job loss, you must reorganize your spending priorities to minimize the risk of default on your mortgage. Keeping your home should be your number one financial goal.

This means you may need to delay payments on unsecured debts, such as credit cards and personal loans, to free up cash for your mortgage. While this can impact your credit, losing your home is a much more severe consequence. Focus on essential monthly bills first.

Here's a sample priority list for your spending:

Top Priority: Housing (mortgage/rent), food, and utilities.

Second Priority: Transportation needed for job searching, and insurance (health, auto).

Lower Priority: Unsecured debts like credit cards, personal loans, and store cards.

Optional Expenses to Cut: Cable TV, gym memberships, entertainment, and subscriptions.

Also, consider assets you can use. A whole life insurance policy might have cash value, or you could sell a second vehicle to generate funds.

How Unemployment Benefits Help Prevent Foreclosure

Unemployment benefits play a direct role in foreclosure prevention by providing you with a source of income to continue making your mortgage payment, even if it's a partial one. This consistent, albeit reduced, income demonstrates to your lender that you are trying to meet your obligations.

This financial support is a key piece of the puzzle when you enter loss mitigation discussions with your lender. It can provide the temporary stability needed to qualify for programs like forbearance or a modified payment plan. Let's delve into these temporary solutions and the importance of communicating with your lender.

Temporary Solutions for Meeting Mortgage Obligations

When your income is reduced, unemployment benefits can provide the temporary assistance needed to bridge the gap. Even if the benefits don't cover your entire mortgage payment, they can supply a significant portion of it, making the shortfall more manageable.

This inflow of available cash is crucial. It can be combined with savings or funds from cutting other expenses to pull together a full payment. In other cases, it allows you to make a partial payment, which is a key step in negotiating with your lender. Showing that you can pay something is better than paying nothing at all.

Temporary solutions include:

Using benefits to make a full payment if possible.

Combining benefits with other funds to meet the mortgage obligation.

Using the income to qualify for plans that let you delay payments or pay a reduced amount for a set period.

Communication With Your Lender About Income Changes

One of the most important steps you can take is to contact your loan servicer as soon as your income changes. Don't wait until you miss a payment. Your mortgage company has heard from people in your situation before and has programs designed to help.

When you call, be prepared to explain your situation honestly. Let them know you've lost your job, have applied for unemployment, and are actively seeking a new job. This proactive communication shows you are a responsible borrower facing a temporary setback. This is the first step in the loss mitigation process.

Your servicer can explain the mortgage relief options available to you. They would much rather work out a temporary solution than go through the expensive and lengthy process of foreclosure. Being upfront and cooperative is your best strategy for getting the help you need.

Impact of Unemployment on Mortgage Forbearance and Deferment Options

Unemployment is a classic reason for a lender to grant mortgage forbearance. Forbearance is a type of mortgage relief where your lender agrees to temporarily reduce or pause your mortgage payments for a specific period. Being unemployed and having a reduced unemployment income is a valid hardship that qualifies many homeowners for this option.

During the forbearance period, you are given time to get back on your feet, for instance by finding a new job, without the immediate threat of foreclosure. Deferment is a similar option where missed payments are moved to the end of your loan term.

Your unemployment income, while limited, can be a factor in these negotiations. It shows you have some ability to pay, which might make a lender more willing to agree to a reduced payment plan rather than a full payment pause. These tools are specifically designed for situations like job loss.

Government Programs Supporting Unemployed Homeowners

Beyond state unemployment benefits, several federal government programs are designed to assist homeowners with foreclosure prevention. These initiatives aim to provide a safety net for those experiencing financial hardship, including job loss.

Programs like the Home Affordable Modification Program, or other affordable modification program options, have helped homeowners find sustainable solutions. These programs, along with emergency funds and state-level initiatives, offer a range of support. The following sections will explore some of these key resources available to you.

Mortgage Forbearance and Relief Options

Mortgage forbearance is a primary form of mortgage relief available to struggling homeowners. It allows you to pause or lower your monthly mortgage payments for a limited time. If you have an FHA-insured loan, your lender must follow specific FHA loss mitigation guidelines, which include offering forbearance for hardships like unemployment.

These options are not automatic forgiveness; you will have to repay the missed amounts eventually. This is typically done through a repayment plan, by adding the amount to the end of your loan, or through a loan modification after the forbearance period ends.

The goal is to give you breathing room to stabilize your finances without falling into foreclosure. Contacting your lender is the first step to see if you qualify for forbearance or other relief options based on your loan type and situation.

Emergency Programs Like the Homeowner Assistance Fund

In response to widespread financial hardship, the federal government established the Homeowner Assistance Fund (HAF). This is one of the key emergency programs designed to help homeowners who are behind on their mortgages and other housing-related expenses.

Administered by states and territories, HAF provides direct financial assistance to eligible homeowners. This money can be used to pay for missed mortgage payments, property taxes, homeowner’s insurance, and utilities. It acts as a source of additional income specifically to prevent foreclosure and displacement.

To access these funds, you typically need to apply through your state's designated HAF program. Eligibility is often based on income and demonstrating a pandemic-related financial hardship, which can include job loss. This can be a powerful tool for catching up on past-due amounts.

State and Federal Initiatives for Preventing Foreclosure

A wide array of state and federal initiatives exist to help homeowners avoid foreclosure. These programs are often tied to the type of loan you have. Major government-sponsored enterprises and federal agencies have their own specific guidelines and relief options.

The U.S. Department of Housing and Urban Development (HUD) is a central hub for assistance, particularly through the Federal Housing Administration (FHA). For conventional loans, the rules may be set by Fannie Mae and Freddie Mac. Even the Department of Agriculture offers help for rural housing loans.

Key entities offering foreclosure prevention initiatives include:

The Federal Housing Administration (FHA) for FHA-insured loans.

Fannie Mae and Freddie Mac for conventional loans they back.

The Department of Veterans Affairs (VA) for VA loans.

The Department of Agriculture (USDA) for rural development loans.

Steps to Take If You Lose Your Job and Fear Foreclosure

If you've lost your job and the risk of foreclosure is causing you anxiety, the most important thing to know is that you have options. The key is to act quickly and decisively. Don't ignore the problem, hoping it will go away. Applying for unemployment benefits is a great first step, but it's not the only one.

Taking control of the situation involves communicating with your lender, exploring options like a loan modification, and getting expert advice from a housing counselor. Let's break down these crucial steps to help you build a plan.

Contacting Your Mortgage Servicer Early

Your very first call after assessing your finances should be to your mortgage servicer. Early communication is the single most effective tool you have to prevent the foreclosure process from starting. Lenders are far more willing to work with borrowers who are proactive and honest about their situation.

Explain that you have experienced a job loss and are facing a financial hardship. They have dedicated departments to handle these situations. Ignoring their letters and calls will only accelerate the path to foreclosure and limit your options.

When you contact them, you open the door to solutions you might not have known existed. Lenders do not want to own your house; the foreclosure process is costly and time-consuming for them too. They have a vested interest in finding a way for you to stay in your home and resume payments.

Exploring Loan Modification and Repayment Plans

When you speak with your lender, ask about their loss mitigation programs. Two common solutions are repayment plans and loan modifications. A repayment plan allows you to catch up on missed payments over a set period by adding a little extra to your regular payment each month.

A loan modification is a more permanent solution for homeowners who can no longer afford their original home loan terms. This process changes the original terms of your mortgage, potentially by lowering the interest rate, extending the loan term, or reducing the principal balance to make your monthly payment more affordable.

These options are designed to create a sustainable payment for your current financial situation. Your lender will require you to submit financial documentation to determine your eligibility, so be prepared to provide information about your income and expenses.

Seeking Professional Housing Counseling

You don't have to navigate this complicated process alone. Seeking professional housing counseling from a HUD-approved agency is one of the smartest moves you can make. These services are often free or very low-cost. A certified housing counselor is an expert in foreclosure prevention options.

Your counselor will review your complete financial situation, help you understand the options your lender offers, and even negotiate with the mortgage company on your behalf. They can help you organize your finances, create a budget, and prepare the paperwork required for assistance programs.

Having an expert advocate in your corner can relieve a significant amount of stress and dramatically improve your chances of a positive outcome. They are a trusted, unbiased resource dedicated to helping you keep your home. You can find a counselor by visiting the HUD website or calling their hotline.

Conclusion

In summary, unemployment benefits can serve as a vital lifeline for homeowners facing the risk of foreclosure. By understanding how to effectively allocate these funds toward mortgage payments and exploring available government programs, unemployed individuals can take proactive steps to safeguard their homes. It’s essential to communicate with lenders and seek financial guidance during these challenging times. Remember, you don’t have to navigate this situation alone—there are resources and professionals available to support you. If you’re uncertain about your options or need assistance, consider reaching out for a free consultation to explore the best path forward for your financial stability.

Frequently Asked Questions

Does receiving unemployment affect my eligibility for mortgage relief programs?

No, receiving unemployment benefits generally does not negatively affect your eligibility for mortgage relief. In fact, it's often a prerequisite, as it demonstrates a qualifying hardship (job loss). Lenders and programs like the Federal Housing Administration use this income information to determine the best FHA loss mitigation options for you.

Are there nonprofit organizations that help unemployed homeowners avoid foreclosure?

Yes, many nonprofit organizations offer free help. HUD-approved agencies provide expert foreclosure prevention counseling. A housing counselor can create a plan, negotiate loss mitigation with your lender, and guide you to resources. The Consumer Financial Protection Bureau website also lists reputable organizations that can assist you.

How long can I stay in my home if paying the mortgage with unemployment benefits?

As long as you use your unemployment benefits to keep your home loan current, you can stay in your home indefinitely. If you fall behind, foreclosure laws vary by state, but the process takes several months. Communicating with your loan servicer can extend this timeline and help you avoid foreclosure court.