Key Highlights

After a job loss, contact your mortgage company before you miss a mortgage payment.

Early action may open a mortgage relief option faster and reduce added stress.

A forbearance period can pause or reduce payments during a temporary setback.

A loan modification may lower payments through changes to the loan term or interest rate.

Some borrowers may qualify for repayment help, payment deferral, or other mortgage assistance.

Acting quickly can help protect your credit and improve your chances of keeping your home.

Introduction

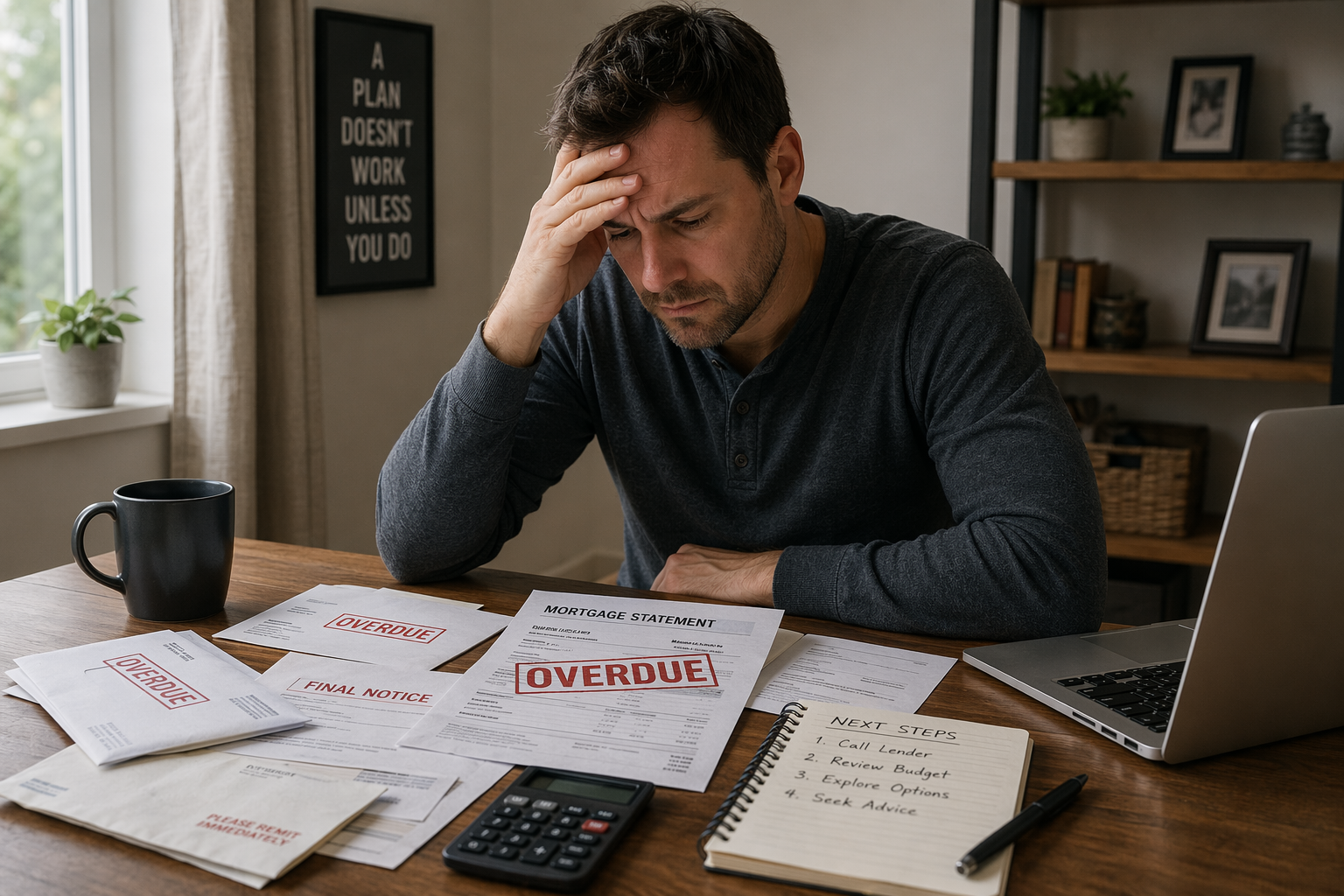

Losing a job can make your next mortgage payment feel much heavier than usual. If that just happened to you, one of the first questions is simple: should you call your mortgage company right away? In most cases, yes. Reaching out early gives you more time to ask about help, explain your situation, and understand what options may be available. You may still have choices, even if your income has suddenly changed. The next sections explain why timing matters.

Why Contacting Your Mortgage Company Promptly Matters After Job Loss

Yes, you should usually call your mortgage company immediately after a job loss, even before you miss a mortgage payment. Your loan does not change just because your income did. Still, early contact can help you learn about possible relief before the account falls behind.

That matters because some solutions, such as loan modification review or temporary payment help, work better when started early. It can also reduce the risk of missed payments hurting your credit score. Before looking at relief programs, focus on the first practical moves you should make.

Immediate Steps to Take Before Missing a Payment

If your savings are running low after a job loss, reach out to your lender or mortgage servicer as soon as you see trouble ahead. Do not wait for the due date to pass. Early contact gives you more room to discuss available assistance programs and next steps.

Before you call, gather the basics so the conversation is clear and useful. Having your contact information, loan details, and a simple explanation ready can save time and help your servicer review your situation faster.

Note the specific date your income changed.

Gather recent details on income, expenses, and savings.

Keep your loan number and contact information nearby.

Ask what mortgage assistance or hardship forms are required.

Write down deadlines and any next steps given by the mortgage servicer.

Once you have these immediate steps covered, it helps to understand why early communication can make a real difference.

Benefits of Early Communication With Lenders

In many cases, it is better to contact your mortgage lender before you actually miss a payment. Early communication shows that your financial hardship is real and that you are trying to address it responsibly. That can help start the loss mitigation process sooner.

Another benefit is that some relief tools may work best before your account becomes more past due. If payments are reported as current during mortgage forbearance or similar arrangements, the impact on your credit score may be smaller than if you simply stop paying without an agreement.

Early communication may help you:

Learn whether mortgage forbearance is available

Ask about a repayment plan or other relief choices

Understand paperwork and timing requirements

Reduce the risk of avoidable credit damage

Now that the timing is clear, the next step is knowing which relief options unemployed borrowers may be offered.

Mortgage Relief Options Available for Unemployed Borrowers

Mortgage companies may offer several forms of mortgage assistance after a job loss. Common options include a forbearance period, a repayment plan, payment deferral, or a loan modification. The right fit depends on whether your hardship is temporary and whether your household has enough steady income to resume payments later.

Some borrowers may also qualify for special programs tied to Fannie Mae, Freddie Mac, FHA, VA, or USDA loans. In some places, state or local help may also exist. To sort through these choices, start with the two most common forms of relief below.

Forbearance and Payment Deferral Explained

Yes, you may be able to get a mortgage payment deferral if you have lost your job, but it usually comes after a forbearance period. Forbearance temporarily reduces or suspends your mortgage payment while you deal with a short-term setback. At the end of the forbearance, you must address the missed payments.

One possible solution is payment deferral. That moves the missed amount to the end of the loan term or end of your loan, instead of requiring immediate repayment. In general, forbearance and deferral are related, but they are not the same thing.

If temporary relief is not enough, a longer-term loan change may be worth exploring next.

Loan Modification Programs for Those Facing Unemployment

If you lose your job and cannot pay, your mortgage does not disappear. The original mortgage loan still exists, but you may be able to request a loan modification or another workout option. A modification is a long-term change to the loan that can make the monthly payment more affordable.

For example, a servicer may adjust the interest rate, extend the loan term, or add overdue amounts to the loan balance. Fannie Mae and Freddie Mac loans may have access to the Flex Modification program, which can reduce payments for eligible borrowers with enough household income to support the new terms.

This option is often different from a repayment plan. A repayment plan helps you catch up over time, while a loan modification changes the loan itself. Because long-term affordability matters, the next section looks at ways to protect your home during hardship.

Protecting Your Home During Financial Hardship

To protect your home during a financial hardship, act early and stay involved. Contact your servicer, complete requested forms, and ask about mortgage assistance that fits your situation. Many homeowners still have options even after a loss of income, especially when the hardship is temporary.

You should also learn your legal rights and keep records of every notice, deadline, and conversation. If foreclosure notices appear, get help fast from a housing counselor or lawyer. The next two sections cover practical foreclosure prevention strategies and the rights you should understand.

Strategies to Avoid Foreclosure After Losing Your Job

Yes, notifying your mortgage lender or mortgage servicer about job loss can help you avoid foreclosure. It does not guarantee a result, but it gives you a better chance to apply for help before the situation gets worse. Ignoring the problem usually limits your choices.

If keeping the home is realistic, ask about solutions that let you stay in place. If it is no longer affordable, other exit options may be less damaging than going through a full foreclosure. A HUD-approved housing counselor can help you compare these paths.

You may want to ask about:

A repayment plan to catch up over time

Temporary forbearance during your job search

A loan modification if household income becomes stable

A short sale if keeping the home is not realistic

A deed in lieu of foreclosure as another last-resort option

Along with these practical choices, it is just as important to know the rules and protections that apply to your mortgage loan.

Understanding Your Legal Rights and Responsibilities

Yes, you do have legal rights if you cannot pay your mortgage because of unemployment. Even if foreclosure begins, you still may have protections and time to pursue alternatives. The process can take a long time in some states, which can give you space to seek help.

At the same time, you still have responsibilities under your mortgage loan unless your servicer approves a different arrangement. That is why written agreements matter. You should understand when payments restart, how missed amounts are handled, and what happens at the end of your loan if amounts are deferred.

It is also smart to review how any relief may appear on your credit report and to ask questions if something is unclear. For general guidance, resources from the Consumer Financial Protection Bureau and a HUD-approved counselor can help you understand your options before making a decision.

Conclusion

In summary, losing a job can be incredibly stressful, but taking prompt action can make a significant difference in your financial situation. By reaching out to your mortgage company as soon as possible, you can explore relief options that may be available to you, such as forbearance or loan modifications. Early communication not only keeps your lender informed but also opens the door to solutions that can help protect your home during this challenging time. Remember, you are not alone in this; seeking assistance is a proactive step towards managing your financial future. If you need more personalized advice, consider reaching out to a financial advisor or counselor who can guide you through this process.

Frequently Asked Questions

Can I qualify for mortgage assistance if I’ve recently lost my job?

You may qualify for mortgage assistance after a recent job loss if you can show financial hardship and meet program rules. Your mortgage company may ask about unemployment benefits, household income, and loan type. Depending on the situation, options may include temporary relief or a loan modification review.

Is it required to tell my mortgage company I’m unemployed before missing payments?

It may not always be strictly required, but telling your mortgage company or mortgage servicer before missed payments is usually the better move. Early notice of a job loss and financial hardship can improve your chances of being reviewed for help before your account becomes more serious.

What should I say when contacting my lender about job loss?

Tell your mortgage lender that you experienced a job loss, share the specific date it happened, and explain that you may struggle with upcoming payments. Have your contact information, loan details, and basic personal information ready. Then ask what hardship options, forms, or next steps apply to your case.