Key Highlights

Ignoring mortgage payments can quickly turn a short-term financial hardship into a serious foreclosure risk.

Your loan servicer usually starts with letters and phone calls after missed payments, not immediate seizure of your home.

Late fees, penalty charges, and credit damage can build fast when mortgage problems go unanswered.

Many homeowners still have options, including a payment plan, forbearance, or loan modification.

Early contact with your lender or a HUD-approved housing counselor can improve your chances of avoiding foreclosure.

Waiting too long can make the entire loan due and limit your solutions.

Introduction

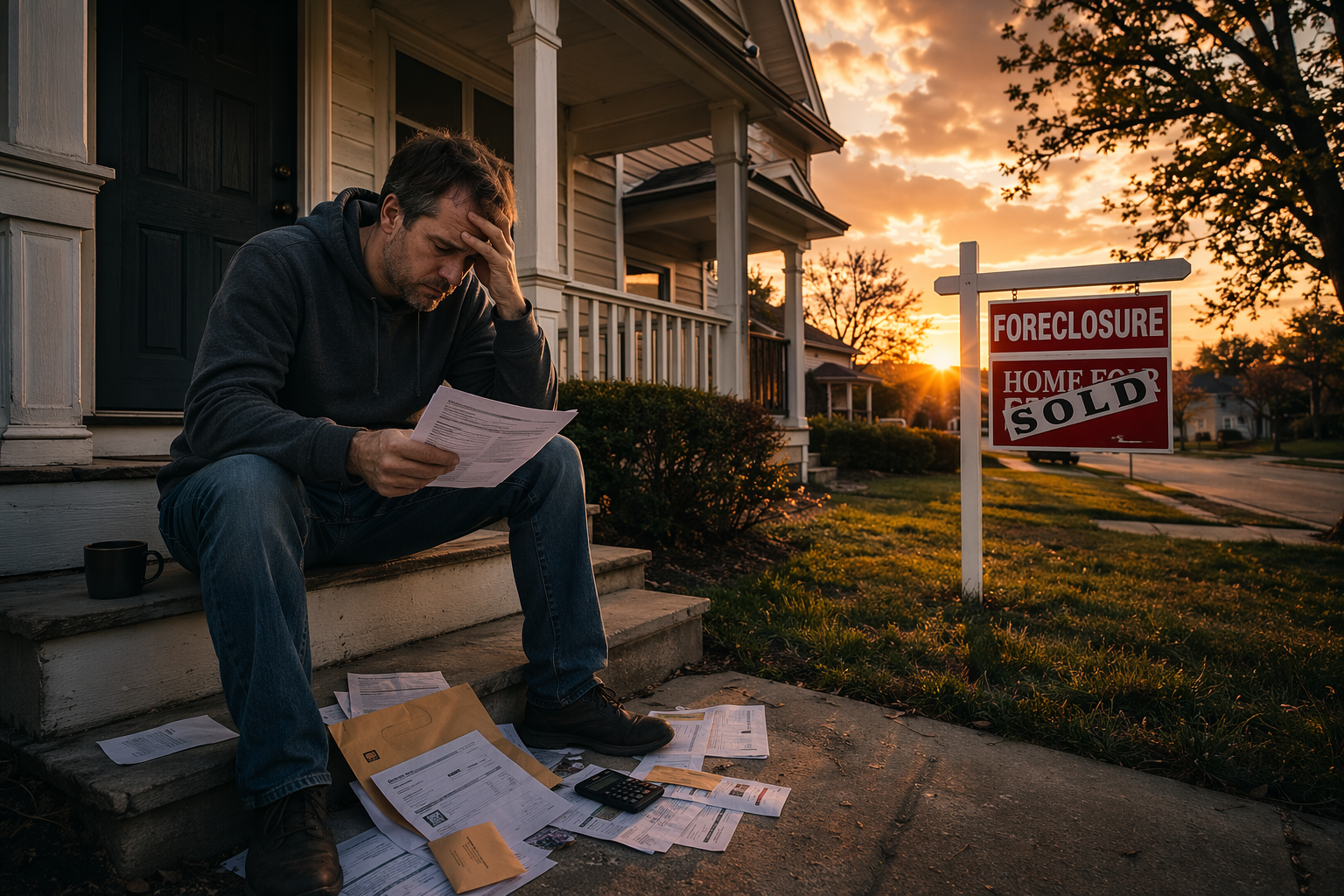

If you are falling behind on mortgage payments, ignoring the issue can put your home at real risk. Many homeowners hope a financial hardship will pass on its own, but silence usually makes things worse. What happens if you ignore mortgage problems instead of addressing them? In most cases, fees rise, options shrink, and a workable payment plan becomes harder to secure. The sooner you act, the better chance you have to protect your home and steady your finances.

The High Cost of Ignoring Mortgage Problems

Ignoring missed payments is risky because mortgage trouble rarely stays small for long. A mortgage lender may begin contact after the first missed due date, and the pressure increases as your account falls further behind. What starts as one skipped payment can grow into larger financial problems.

Over time, foreclosure becomes more likely. If no arrangement is made, the entire loan may become due, and that is a much harder problem to solve. To understand why people wait too long, it helps to look at the early warning signs first.

Why Homeowners Often Overlook Early Warning Signs

At first, many people think they just need a little time. You may expect your income to recover soon, or believe you can catch up after missing one month of mortgage payments. Because of that, the problem can feel temporary rather than urgent.

Then the signs start stacking up. It may become harder to cover regular payments, monthly bills, groceries, or credit card balances. If that pressure lasts for any period of time, it usually points to deeper financial difficulties rather than a one-time setback.

Your loan servicer may also send letters or try to call early in the process. Some homeowners avoid those messages because they feel embarrassed or overwhelmed. Yet those first notices often contain useful information about help, deadlines, and ways to prevent the account from getting worse.

Psychological Barriers to Addressing Mortgage Issues

For many homeowners, the biggest barrier is not the lender. It is denial. When mortgage payments become hard to manage, people often hope the issue will disappear before anyone notices. That reaction is common, especially during financial hardship.

Stress makes the problem heavier. You may feel shame, fear, or panic each time a letter arrives. Instead of opening mail or returning a call, some people freeze. That delay can lead to more missed deadlines and fewer options.

Looking away does not protect your financial future. It usually gives fees, delinquent status, and foreclosure risk more time to grow. A hard conversation today is easier than dealing with legal action months later. Facing the problem early is often the safest move you can make.

Misconceptions About Mortgage Lenders and Flexibility

A common myth is that a mortgage lender wants your house right away. In reality, the compiled guidance says lenders do not want your house and often have options for borrowers going through a financial crisis. That is why early contact matters.

Another mistake is assuming silence buys you flexibility. It usually does the opposite. A loan servicer may offer help in early notices, but if you ignore those messages, the process can move toward attorneys, added costs, and formal foreclosure steps.

Keep these points in mind:

Lenders often contact you early to discuss options, not just to threaten legal action.

Ignoring mail does not stop deadlines or make foreclosure laws disappear.

If documents are confusing, getting legal advice or help from a housing counselor can protect you.

Common Triggers That Lead to Mortgage Default

Mortgage default usually grows out of pressure that builds over time. When mortgage payments compete with groceries, credit cards, taxes, or other monthly bills, even careful households can face financial hardship. The problem is often not one bad choice but a sudden change in circumstances.

Common triggers include job loss, medical expenses, divorce, and payment increases. Each one can make it harder to stay current and increase the risk of loss of your home. The next sections break down how these pressures often unfold.

Job Loss and Income Disruption

Job loss is one of the clearest paths to mortgage trouble. When a paycheck stops, your mortgage payments do not pause with it. Even a short income disruption can throw off a budget that once worked fine.

Soon after, savings may go toward groceries, utilities, or healthcare. That can leave less cash for the mortgage loan. If the setback lasts more than a month or two, many borrowers start choosing which bills to pay first, and default becomes a real threat.

Financial difficulties tied to job loss can also create emotional strain. You may think a new job is right around the corner, so you wait. But waiting can push you deeper behind. Early contact with the lender or loan servicer is often the best way to buy time and explore relief options.

Unexpected Medical Expenses or Emergencies

Medical expenses can disrupt a household fast. A hospital stay, urgent treatment, or another emergency can create large bills at the same time income drops. When that happens, mortgage payments may no longer fit easily into your budget.

Unlike planned costs, emergencies do not give you time to prepare. You may start relying on credit cards for groceries or other monthly bills, which is one of the warning signs mentioned in the compiled guidance. That often signals growing financial hardship.

If you are choosing between immediate care and the mortgage, the situation is already serious. It does not mean you have failed. It means you need to act quickly. Lenders, servicers, and housing counselors may be able to help you review options before the account becomes deeply delinquent.

Adjustable-Rate Mortgage Payment Increases

Sometimes the trigger is not a lost job or emergency. It is a payment increase. If you have an adjustable-rate mortgage, changing interest rates can raise your monthly payment beyond what you expected when you first signed the loan.

For a homeowner already managing tight cash flow, even a moderate increase can upset the whole budget. Higher housing costs may clash with taxes, insurance, food, transportation, and other bills. That is when once-manageable home mortgages start to feel unstable.

If you notice your monthly payment rising and your finances tightening, treat it as an early warning sign. Waiting until you miss several payments makes the problem harder to fix. Reaching out while you are still partly current may open more room for a modification or another form of relief.

Immediate Consequences of Missed Mortgage Payments

Missed payments trigger consequences quickly. Your mortgage servicer may send letters, start phone outreach, and add late charges once the due date passes and the account becomes delinquent. This early stage can feel manageable, but it is often the moment when action matters most.

If you keep ignoring the debt, the foreclosure process becomes more likely. Later mail may include warnings tied to legal action, and your failure to open or answer notices does not stop the case. The first costs appear fast, starting with fees and penalties.

Late Fees and Penalty Charges

One missed due date can cost more than you expect. Mortgage payments are typically due on the first of the month and considered late after the 15th. At that point, late fees, penalty charges, and written correspondence may begin on your mortgage loan.

The longer you wait, the more expensive it gets. A single past-due payment can become two, then three, and each missed month adds to the amount needed to catch up. After months of nonpayment, attorney fees may also become part of the delinquency.

That is why ignoring the issue is so dangerous. What looked like one temporary shortfall can turn into a much larger bill. Reinstating the loan gets harder as fees pile up, especially if you have not made any arrangements with the lender or servicer during the early stages.

Negative Impact on Credit Scores

Yes, missed mortgage payments can affect much more than your home loan. Once your account becomes delinquent and nonpayment is reported, your credit scores can drop sharply. That damage may stay with you for years and affect how future creditors view you.

Lower credit can make everyday finances harder. It may affect your ability to borrow, refinance, or even rent a home later. If you are already struggling with monthly bills, a credit setback can add another layer of pressure across the rest of your financial life.

This is one reason ignoring mortgage trouble is considered such a risky mistake. Even if foreclosure has not started yet, your financial profile may already be worsening. Protecting your credit scores often begins with early communication and a serious effort to address the delinquent account.

Collection Activity and Frequent Lender Contact

When payments are missed, contact usually increases. Your loan servicer or lender may send written correspondence, make phone calls, and ask you to explain the situation. The purpose early on is often to discuss why payments stopped and whether a solution is possible.

It is important to take those contacts seriously. The compiled guidance says you should not ignore the letters and should take the phone calls. Early notices may include information about foreclosure prevention options, deadlines, and ways to bring the account current.

Be careful, though. One source notes that scams can appear by phone or email, with someone pretending to be your lender. Genuine notices often come through the mail. If you are unsure, contact your servicer directly using trusted account information rather than responding to an unexpected message.

How Ignoring Mortgage Problems Escalates Financial Risk

Ignoring mortgage problems raises the financial stakes month by month. Missed payments do not sit still. They can lead to added fees, attorney costs, and compounding debt, making future loan repayments harder to manage. What began as a short setback can become a long-term burden.

As pressure builds, foreclosure risk increases and bankruptcy may enter the picture. Not responding can damage your credit, drain savings, and reduce the choices you have left. To see why, start with how the balance itself keeps growing.

Rising Interest Accrual and Compounding Debt

When you stop making mortgage payments, the unpaid amount does not freeze. Charges continue to build, and in many cases interest still accrues during temporary relief periods such as forbearance. That means the balance you need to address can grow while you wait.

As financial difficulties continue, the gap becomes harder to close. One missed payment turns into several, then added fees, then attorney costs if the file moves forward. This pattern creates compounding debt, even without taking on a new loan.

Rising interest rates can also make existing pressure worse, especially for borrowers with adjustable-rate loans. The result is a harder path back to current status and a higher chance of default. Responding early can keep the amount owed from growing beyond what your budget can realistically handle.

Damage to Long-Term Financial Goals

Ignoring mortgage issues can affect far more than one monthly bill. It can disrupt your financial goals for years. Saving, rebuilding credit, buying again later, or protecting your family budget all become harder when the account keeps falling behind.

Foreclosure is especially damaging because it can lead to the loss of your home and the loss of progress you spent years building. That includes the stability of staying put, the value tied to the property, and your standing with future lenders.

Even before a foreclosure sale, uncertainty can change your decisions. You may stop planning for the future and focus only on getting through the week. That is understandable, but it is also why early action matters. Working with the lender sooner can help preserve options you may need later.

Increased Likelihood of Bankruptcy

When mortgage trouble grows unchecked, bankruptcy can become part of the conversation. It is not the automatic next step, but severe delinquent debt, added fees, and a foreclosure process already in motion can push households toward extreme choices.

This risk increases when a borrower has waited too long to pursue a payment plan or other workout option. Once the mortgage loan becomes deeply past due, the amount needed to catch up may be more than the household can manage. At that stage, every option feels more painful.

There are consequences to letting things reach this point, whether the missed payments were driven by hardship or a strategic choice. A foreclosure and a bankruptcy can both leave lasting marks on your finances and future housing opportunities. Acting early helps reduce the odds of facing both at once.

The Road to Foreclosure: A Step-By-Step Breakdown

Foreclosure does not happen overnight, but it does move forward when a borrower stays in default. The mortgage lender usually starts with notices and contact attempts, then escalates if no payment or arrangement is made. Ignoring debt absolutely can make foreclosure more likely on your home.

The exact time frame varies by state, yet the pattern is similar: delinquency, formal notice, attorney involvement, sale, and possible removal from the property. Understanding each stage can help you act before legal action reaches the final steps.

Notice of Default and Its Implications

After enough days of nonpayment, the lender may issue a formal warning. One source explains that after the third missed payment, you may receive a letter stating how much you are delinquent and giving you 30 days to bring the mortgage current. This is often called a notice of default, demand letter, or notice to accelerate.

That letter matters. It signals that foreclosure could follow if you do not pay the required amount or make arrangements by the deadline. At this point, the lender is no longer just reminding you. The file is moving closer to legal action.

Even here, you may still have time to respond. The guidance makes clear that you can often work something out before the sale stage. But if you do nothing, the situation can shift from warnings to attorneys, added costs, and a much more serious foreclosure track.

Pre-Foreclosure Period: What Happens Next

Pre-foreclosure is the stretch after you fall behind but before the property is sold. During this time, the mortgage servicer usually increases collection activity through letters and phone calls. The key question is simple: will you resume regular payments, make an arrangement, or continue ignoring the account?

The time frame varies by state and by loan, but the compiled guidance outlines a common path. Acting during this period can still help you avoid the final sale stage.

If you are struggling, the immediate step is to answer the mortgage servicer, review your mail, and ask about available help. A HUD-approved housing counselor can also help you understand timelines, organize finances, and communicate with the servicer.

Auction and Eviction: Final Steps in Foreclosure

If no solution is reached, the foreclosure process can end in a sale. The attorney may schedule an auction, sometimes called a sheriff or public trustee sale, depending on the state. You may be notified by mail, by a notice posted at your door, or through a local paper.

This sale is a major turning point. It is not always the same as the move-out date, but it means the end is close. Up to the auction date, you may still be able to make arrangements or pay the total amount owed, including attorney fees, depending on the circumstances.

After the sale, some states allow a redemption period. After that, removal from the property may follow, and a writ of possession can become part of the final eviction stage. In simple terms, if you ignore mortgage problems long enough, you can lose both the home and control over the timing of your departure.

How Mortgage Default Affects Homeowners’ Future Opportunities

Mortgage default does not end when you leave the property. Its effects can follow you into future borrowing, renting, and homeownership plans. Credit damage, foreclosure history, and unresolved debt can all limit what lenders or landlords are willing to offer.

For home buyers, this can mean delays, higher costs, or outright denials years later. A period of financial hardship may pass, but the record of default can keep shaping your options. The next sections show where those limits often appear.

Challenges in Buying a Home After Foreclosure

A foreclosure can make buying again much harder. Home buyers with damaged credit scores often face extra scrutiny from every lender they approach. Even if your income improves later, the history of missed housing payments can remain a serious concern.

That matters for two reasons. First, a foreclosure can reduce your immediate chance of keeping your home because options narrow as the case moves forward. Second, if the property is lost, the same record may limit your next attempt to buy.

Lenders want signs that future payments will be stable. A foreclosure suggests the opposite, even when the original cause was genuine hardship. This is why early action is so important. Protecting your current home can also protect your ability to become a homeowner again later.

Limited Access to Credit and Higher Interest Rates

Credit problems rarely stay in one lane. If you fall behind on mortgage payments, future credit may become harder to obtain and more expensive when you do qualify. A lender may see the delinquency as a sign of elevated risk.

That often leads to higher interest rates, stricter terms, or fewer available products. In practical terms, financial hardship today can raise the cost of borrowing tomorrow. That includes later home loans and other forms of credit that support everyday life.

This is another way silence can hurt your future. By not responding early, you increase the chance that the mortgage problem spreads into a wider borrowing problem. Protecting your standing with one loan can help preserve access and affordability across the rest of your financial picture.

Loss of Home Equity and Savings

Foreclosure can also erase value you built over time. If you have home equity, losing the property may mean losing a major financial asset. That is especially painful when years of mortgage loan payments created that value.

Savings often suffer too. Many people use cash reserves trying to stay afloat while also paying late charges, attorney costs, and other bills. If the effort still ends in foreclosure, both the house and the safety cushion may be gone.

In the long run, that loss can delay recovery. Without home equity or savings, it becomes harder to rent, buy again, handle emergencies, or rebuild financial confidence. That is why the real cost of ignoring mortgage trouble reaches far beyond the month when the first payment was missed.

Options for Homeowners Struggling With Payments

If you are behind, you may still have several ways to respond. Common options include a payment plan, loan modification, and forbearance. These tools are meant to help borrowers facing financial hardship before foreclosure becomes unavoidable.

If keeping the home is no longer realistic, selling may be another path. In some cases, a real estate agent can help you move faster than waiting for the legal process to finish. The best option depends on how long your setback is expected to last.

Loan Modification Programs and Qualifications

A loan modification changes the terms of your loan so the payment fits your budget better. This option is often used when the problem is not short-term, such as after a job change, divorce, or lasting increase in expenses. The goal is to make the monthly payment more manageable.

Your loan servicer is usually the first place to ask about qualifications. The compiled information does not list exact approval standards, but it makes clear that lenders and servicers may have options for borrowers who contact them early and explain their hardship.

If you want to stay in your home and can no longer afford the current mortgage payments, a loan modification may be worth discussing. It is not automatic, but it can offer a path forward before the account reaches a deeper stage of default or foreclosure.

Forbearance and Repayment Plans Explained

Forbearance gives you a pause or reduction in mortgage payments during temporary hardship. It usually lasts for a set period of time rather than forever. This can help if the problem is short-term, such as temporary unemployment or another limited disruption.

A repayment plan works differently. If you are only a few payments behind and think you can recover, the loan servicer may allow smaller catch-up steps over time instead of demanding everything at once. This can help you restore the account without an immediate lump sum.

Both options require communication. In many cases, interest may still accrue during forbearance, and missed amounts eventually come due. That is why you should ask early about how the terms work, what the end date is, and what your payment obligations will be once the relief period ends.

Selling Your Home to Avoid Foreclosure

Sometimes keeping the property is no longer the best fit. In that case, selling your home may be better than waiting for foreclosure to play out. A sale can give you more control over timing and may reduce some of the damage compared with losing the property through a forced process.

Working with a real estate agent may help you move more quickly and understand the market. If the home is worth less than what you owe, you may also need to ask the mortgage lender about a short sale. That requires lender approval because the sale price may not cover the full balance.

Is selling your home better than waiting for foreclosure? In many cases, yes, because it can preserve more dignity, more choice, and sometimes more of your finances. The best way forward depends on your equity, urgency, and whether you still want to stay.

Proactive Steps to Prevent Mortgage Problems

If you are worried about falling behind, act before the situation becomes severe. Strong budgeting, better financial management, and early contact with the lender can reduce the chance that one bad month turns into a long default. Quick action keeps more options open.

You do not have to solve everything alone. A housing counselor can help you review your finances, understand notices, and ask about a payment plan or other relief. The next steps are practical and often easier than people expect.

Early Communication With Lenders

If you are struggling, the best way to start is simple: contact your lender or loan servicer as soon as you realize there is a problem. Early communication can make a major difference because the account may still be in a stage where more options are available.

You do not need a perfect script. Explain why mortgage payments have become difficult, what changed, and whether the issue is temporary or longer lasting. The compiled guidance makes clear that lenders may have foreclosure prevention options and often prefer to discuss solutions before things worsen.

Waiting rarely helps. Once letters go unanswered and deadlines pass, the file can move closer to attorneys and formal foreclosure steps. Speaking up early gives you a better chance to ask questions, understand timelines, and find a workable path before the problem becomes much more expensive.

Budgeting and Financial Management Strategies

A tight budget can feel discouraging, but clear financial management helps you see what is possible. The compiled guidance says that after healthcare, keeping your house should be a top priority. That means reviewing monthly bills and cutting optional costs where you can.

Start with practical moves:

Cancel or pause optional spending such as entertainment, memberships, or premium services.

Review whether assets could be sold for cash to help catch up.

Consider extra income from another job in the household, if possible.

These steps may not solve every financial hardship, but they show effort and create breathing room. They can also support a discussion about a payment plan with your lender or servicer. A realistic budget is often the first tool you need before any long-term solution can work.

Working With Certified Housing Counselors

You do not need to face this alone. A certified housing counselor can help you understand your options, organize paperwork, and communicate with the lender. The compiled information points readers to HUD-approved counseling agencies that provide free or very low-cost help.

This support can be especially useful when financial difficulties feel overwhelming. A housing counselor can help you understand foreclosure prevention options, review your budget, and explain what notices from the lender mean. In some cases, they may also assist in negotiations.

HUD and other government-backed resources are available for homeowners who need guidance. If your loan is FHA-insured, the Federal Housing Administration also offers loss mitigation resources. Reaching out early can turn confusion into a plan, which is often exactly what stressed borrowers need most.

Risks of Strategic Default and Ignoring Debts

Some borrowers think about strategic default, meaning they choose to stop paying a mortgage loan even when they might still have other options. That approach can carry serious consequences, especially once the account becomes delinquent and the lender follows state foreclosure laws.

Ignoring debts does not make the legal process disappear. It can lead to notices, added costs, credit damage, and possible legal action. Beyond the money, strategic default can also affect your reputation in the housing market and your future ability to secure stable housing.

Legal Ramifications and Potential Lawsuits

Strategic default is not just a financial choice. It can trigger legal action under your state’s foreclosure laws. Once you stop paying, the lender may issue formal notice, move the case through attorneys, and follow the steps required to enforce the mortgage agreement.

The compiled guidance stresses that mail from the lender may later include important notices of pending legal action. Ignoring them is not a defense. Your failure to open the notice will not excuse you in foreclosure court, and deadlines still apply whether or not you respond.

From a practical view, this means a creditor can keep advancing the case while costs rise. Attorney fees may be added to what you owe, and the path toward sale becomes more direct. Strategic default may seem simple at first, but the legal consequences can be lasting and expensive.

Moral and Community Impacts

Foreclosure affects more than one household. It can ripple through a community by creating instability, stress, and turnover. When homes move through distress, neighbors notice, and local confidence can weaken, especially when several homeowners are struggling at once.

That said, it is important to separate hardship from choice. Many homeowners face foreclosure because of job loss, medical problems, divorce, or another genuine financial hardship. They are not acting irresponsibly. They are dealing with circumstances that changed faster than their budget could adapt.

Still, choosing to ignore the problem can deepen the damage for everyone involved. Open communication, counseling, and a serious effort to resolve the issue help protect not only your own future but also the stability of the neighborhood around you.

Difficulty in Securing Future Housing

Yes, ignoring mortgage strategy can hurt your chances of keeping your home and can also make future housing harder to secure. A foreclosure or major delinquency can raise red flags for landlords just as it does for mortgage lenders.

Many renters are screened for payment history and overall credit profile. If a landlord sees missed mortgage payments, foreclosure, or bankruptcy, that may suggest risk. Even if you are ready to move on, the record may follow you into the next application.

This is why the cost of inaction stretches beyond the current property. Losing a home can be followed by difficulty renting the next one. Protecting your standing now, even during hardship, can improve your housing options later and reduce how long the disruption lasts.

Conclusion

In conclusion, ignoring mortgage problems can lead to devastating financial consequences that extend far beyond just missed payments. Homeowners often find themselves trapped in a cycle of rising debt and deteriorating credit scores, making it increasingly difficult to regain control of their finances. By addressing issues early on, communicating with lenders, and seeking professional advice, you can prevent the downward spiral into foreclosure and safeguard your future opportunities. Remember, taking proactive steps now can save you from long-term repercussions. If you’re facing challenges with your mortgage payments, don’t hesitate to reach out for help—your financial well-being is worth it.

Frequently Asked Questions

What is the first thing I should do if I can’t make my mortgage payment?

The first step is early communication with your lender or loan servicer. As soon as you know mortgage payments will be difficult, explain the financial hardship and ask what options may be available. Acting quickly can help preserve choices and prevent the account from getting worse.

Can ignoring mortgage payments affect other areas of my finances?

Yes. Missed payments can make your mortgage delinquent, damage credit scores, and make future borrowing or renting harder. If a lender reports the nonpayment, the effects can spread well beyond the home loan. During financial hardship, that added credit damage can make recovery slower.

Is selling my home better than waiting for foreclosure?

In many cases, selling your home is better than waiting for foreclosure because it gives you more control and may reduce long-term damage. A real estate agent can help you move faster. If mortgage payments are no longer sustainable, this may be the best way to avoid a forced sale.